Smartphone Market Share 2026 vs 2025: Top Brands Compared

Zoheb / Important, News And Rumors

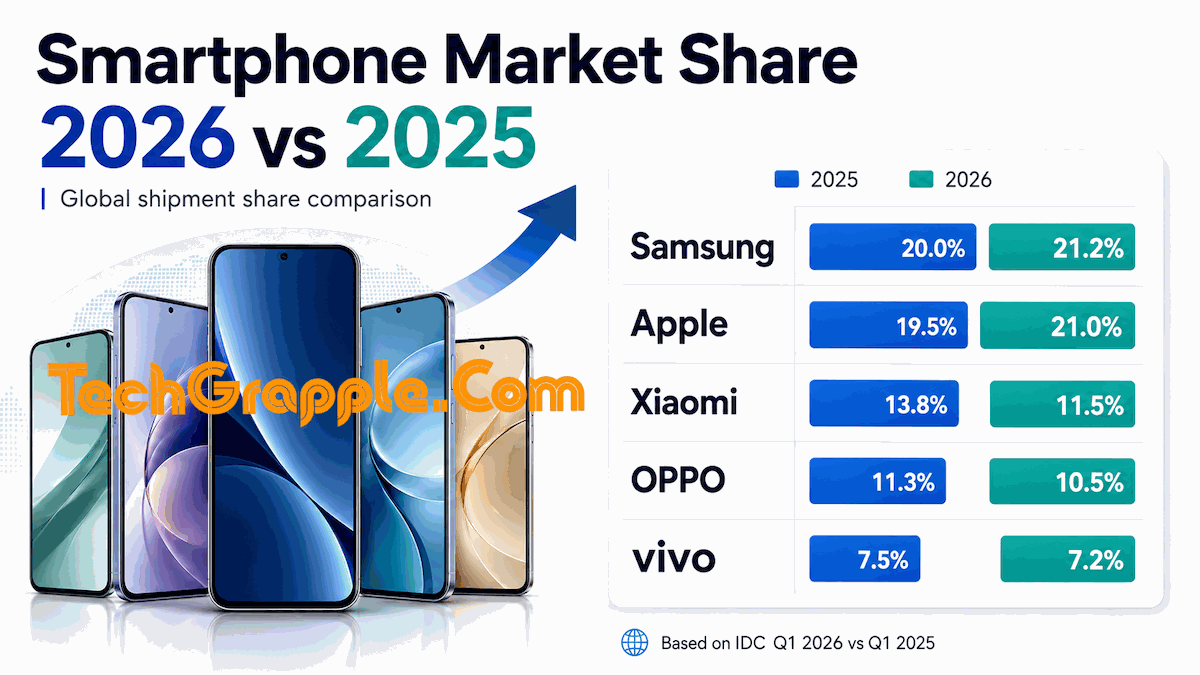

Global smartphone shipment market research • updated May 19, 2026

The 2026 smartphone market share story is not a normal “new winner” cycle. It is a supply-cost cycle. Samsung and Apple expanded share in Q1 2026 while the overall market contracted, because premium-focused vendors were better positioned to absorb memory-cost pressure and secure component supply. Xiaomi, OPPO and vivo remained major global players, but their Q1 shares declined as lower-price segments became harder to serve profitably.

- 293.8M smartphones shipped worldwide in Q1 2026 IDC: down 2.9% year over year

- 21.2% Samsung Q1 2026 share No. 1 by IDC shipment share

- 21.0% Apple Q1 2026 share Only 0.2 percentage points behind Samsung

- +2.7 pp Samsung + Apple combined share gain 42.2% in Q1 2026 vs 39.5% in Q1 2025

2026 vs 2025: the direct market-share comparison

IDC’s Q1 2026 data shows a market that became more concentrated at the top. Samsung increased from 20.0% to 21.2%, while Apple increased from 19.5% to 21.0%. Xiaomi’s share fell from 13.8% to 11.5%, OPPO declined from 11.3% to 10.5%, and vivo moved from 7.5% to 7.2%. The “Others” category increased from 27.8% to 28.6%, partly reflecting the long tail of regional and specialist brands.

- Q1 2025

- Q1 2026

- Share gain

- Share loss

Detailed data table

| Vendor | Q1 2025 shipments | Q1 2026 shipments | Shipment growth |

|---|---|---|---|

| Samsung | 60.6M | 62.4M | +2.9% |

| Apple | 59.1M | 61.8M | +4.4% |

| Xiaomi | 41.8M | 33.8M | -19.1% |

| OPPO | 34.1M | 30.7M | -9.9% |

| vivo | 22.7M | 21.2M | -6.9% |

| Others | 84.3M | 84.0M | -0.3% |

| Total market | 302.6M | 293.8M | -2.9% |

What changed in 2026?

- Samsung and Apple gained share while the market shrank. Samsung’s Q1 2026 share rose to 21.2%, and Apple’s rose to 21.0%. Together, they represented 42.2% of Q1 2026 shipments, compared with 39.5% in Q1 2025.

- Xiaomi had the sharpest top-five decline. Its shipments fell from 41.8 million to 33.8 million, a 19.1% year-over-year drop, and its share declined by 2.3 percentage points.

- OPPO and vivo remained top-five vendors but lost share. OPPO declined by 0.8 percentage points, while vivo declined by 0.3 percentage points. Both were affected by weaker low-end demand and intense competition in China and emerging markets.

- The “Others” category gained share despite slightly lower shipments. That means the long tail did not grow much in absolute units, but it took a larger slice because the overall market contracted.

Why the market is under pressure

The main structural issue in 2026 is memory supply. DRAM and NAND costs rose sharply as AI data-center demand absorbed more memory capacity, increasing bill-of-materials pressure for smartphone makers. This pressure is especially painful in entry-level and low-midrange smartphones, where memory represents a larger portion of device cost and vendors have less room to absorb price increases.

Premium-heavy vendors such as Apple and Samsung have stronger purchasing leverage, higher average selling prices, and larger flagship demand pools. That does not make them immune to cost inflation, but it helps them defend margins and shipment share better than brands that rely heavily on sub-$200 models.

2025 full-year context

Full-year 2025 was stronger than the start of 2026. Counterpoint, reported by Reuters, said global smartphone shipments grew 2% in 2025, with Apple leading at 20% share, Samsung at 19%, and Xiaomi at 13%. Omdia similarly reported that 2025 shipments grew 2% to about 1.25 billion units, the highest annual level since 2021, with Apple delivering a record annual volume and Samsung rebounding after several years of declines.

That makes the Q1 2026 reversal important: the market moved from a modest recovery year in 2025 into a supply-cost squeeze in early 2026. The likely impact is less about one brand suddenly becoming dominant and more about a wider gap between premium-scale vendors and low-price-volume vendors.

Bottom line

The 2026 smartphone market is moving toward a more premium, supply-constrained structure. In Q1 2026, Samsung narrowly led global shipment share, Apple nearly matched it, and both gained share from 2025. Xiaomi, OPPO and vivo remained globally important, but their declines show how rising component costs can quickly pressure brands with heavy exposure to lower-price segments. Until memory prices stabilize and full-year 2026 data is complete, the most truthful conclusion is that 2026 is not just a market-share race; it is a resilience test for smartphone supply chains, pricing power and portfolio mix.

Analyst-source cross-check

| Source | Period | Headline result | Best use in this article |

|---|---|---|---|

| IDC | Q1 2026 vs Q1 2025 | 293.8M shipments in Q1 2026, down 2.9% YoY; Samsung 21.2%, Apple 21.0% | Primary chart and table dataset |

| Omdia | Q1 2026 vs Q1 2025 | 298.5M shipments in Q1 2026, up 1% YoY; Samsung 22%, Apple 20% | Cross-check showing similar ranking but different total/growth methodology |

| Counterpoint via Reuters | Full-year 2025 | 2025 shipments grew 2%; Apple 20%, Samsung 19%, Xiaomi 13% | Full-year 2025 context, not the main Q1 comparison |

| Omdia | Full-year 2025 | 2025 shipments grew 2% to 1.25B units; Apple and Samsung both reached new highs | Full-year 2025 context and trend validation |

Why sources differ: research firms use different channel checks, shipment definitions, vendor groupings, and reporting dates. For example, Omdia’s Q1 2026 OPPO figure includes OnePlus and realme, while IDC’s table uses its own parent-company methodology. The safest reading is the shared trend: Apple and Samsung are stronger in 2026, while memory-cost pressure is hurting lower-price-volume brands.